Consumer RAM prices (Memory) have undergone a significant market correction in late 2025 and early 2026, ending a prolonged period of historic lows. Following 90 days of aggressive volatility, standard DDR4 and DDR5 memory kits are now trading at roughly 3-4x (400% Higher!!) their Q3 2025 valuations.

If you want to buy RAM, the better option is to buy a Mini PC, rather than just RAM. Mini PC prices haven’t caught up with the RAM Crisis due to excess inventory from mid 2025. And you can get a Mini PC for almost the price of Ram Only! (which is crazy, but will change soon). Here are our top Mini PC Recommendations For 2026.

Whether you want to upgrade your Mini PC, Build a Homelab or AI Server, or simply a powerful Gaming PC, budgeting for RAM is one of the first things you should do in 2026.

This article analyzes pricing data from major retail channels over the last 12 months to identify the structural causes behind this surge. The data indicates that a confluence of supply chain constraints—specifically the reallocation of wafer capacity to High Bandwidth Memory (HBM)—and a shift in consumer usage patterns has created a severe supply-demand imbalance.

Market Data: Quantifying the Surge

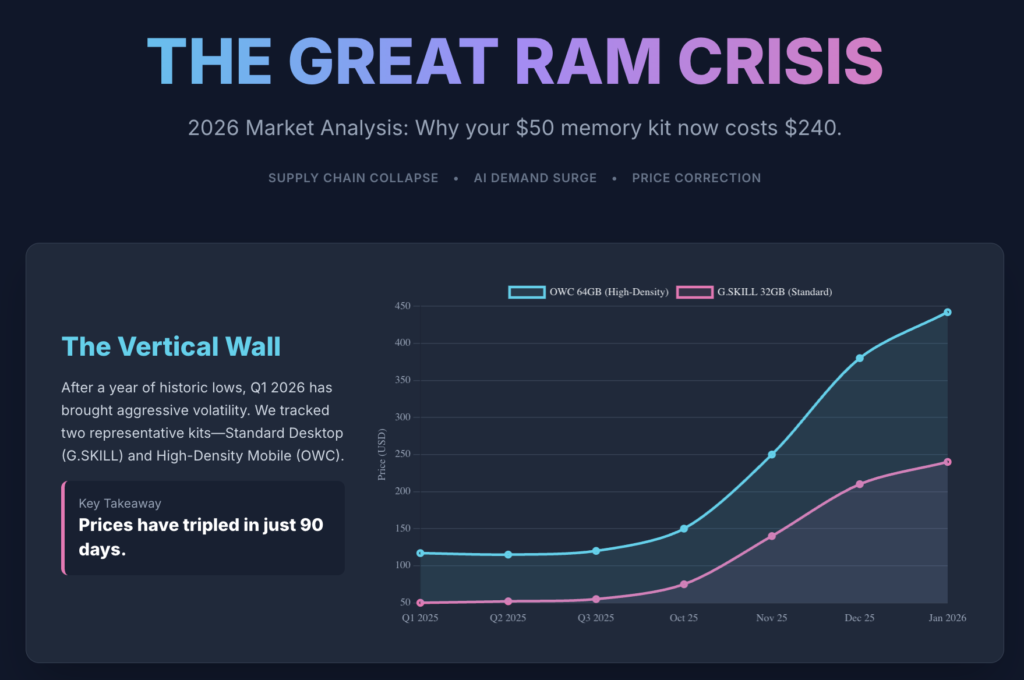

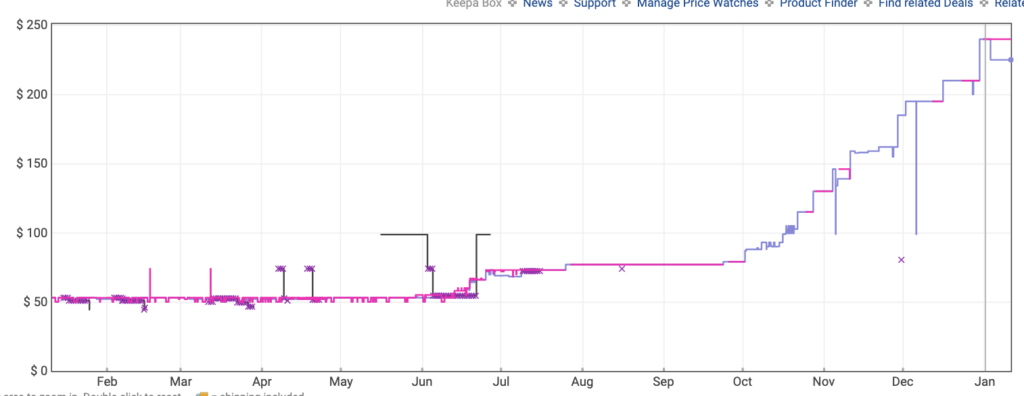

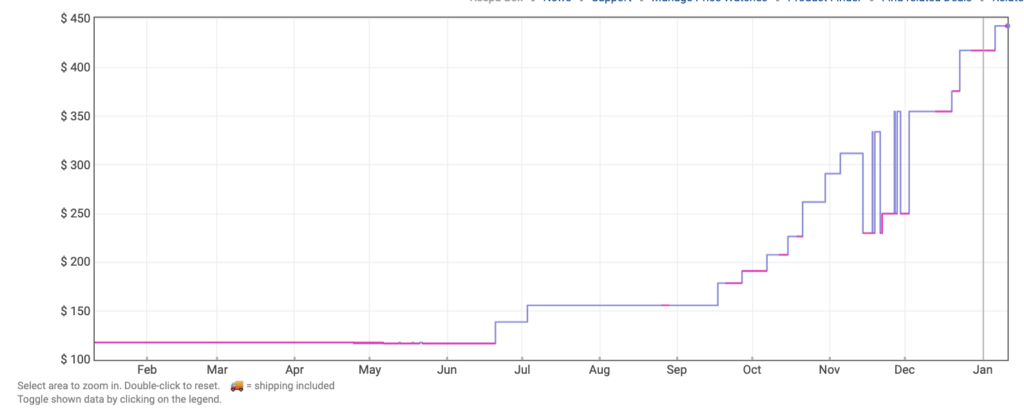

To illustrate the extent of the price correction, we tracked the pricing history of two representative memory kits: a standard desktop kit (G.SKILL) and a high-capacity SODIMM kit (OWC) often used in creative workstations.

Data Point A: Standard Desktop Memory

Product: G.SKILL Ripjaws V Series 32GB (2 x 16GB) DDR4

- Q1 2025 Average: ~$50.00

- Q1 2026 Current: ~$240.00

- Net Change: +380%

This segment has seen the most drastic percentage increase. Previously positioned as an entry-level commodity, 32GB kits have effectively moved into the premium pricing tier, disrupting the bill-of-materials (BOM) for mid-range system integrators.

Data Point B: High-Density Mobile Memory

Product: OWC 64GB (2 x 32GB) 2666MHz DDR4 SO-DIMM

- Q1 2025 Average: ~$117.00

- Q1 2026 Current: ~$442.00

- Net Change: +277%

The steep rise in 64GB kit pricing correlates directly with the increased demand for local virtualization and AI inference workloads, which are memory-intensive.

Core Drivers of the 2026 Price Correction

The current pricing environment is not the result of a single temporary shortage but rather three structural shifts in the semiconductor industry.

1. The “System as VRAM” Shift

The widespread adoption of local Large Language Models (LLMs) in late 2025 has fundamentally altered consumer memory requirements. Efficient local models, such as Llama-4 and Mistral-Local, require significant memory overhead to store model weights and context windows.

For consumers running 70B parameter models, 64GB or 96GB of system RAM acts as a necessary buffer for GPU VRAM. This has transformed high-capacity RAM from a niche requirement for video editors into a standard requirement for prosumers and developers, draining global inventory of high-density modules.

2. Supply Chain Reallocation to HBM

The most significant supply-side factor is the industry pivot toward High Bandwidth Memory (HBM) to service data center demand.

- The Constraint: HBM production is silicon-intensive. Industry reports indicate that HBM consumes approximately 3x the wafer capacity of standard DDR5 per gigabit of capacity.

- The Impact: Major foundries (Samsung, SK Hynix, Micron) have reallocated production lines to prioritize high-margin HBM for enterprise GPUs. This has resulted in a net reduction in wafer starts for consumer-grade DDR4 and DDR5, creating a physical scarcity of standard memory dies.

3. DDR4 “End of Life” Phase-Out

While demand remains high for legacy platforms (AM4, older laptops), manufacturers have aggressively scaled back DDR4 production to force the transition to DDR5. This mismatch—falling supply against steady demand—has created a “legacy tax,” where older technology is now trading at a premium due to scarcity.

The Ripple Effect: Impact on System Integrators and DIY Budgets

The surge in memory pricing has disproportionately affected the sub-$1,000 PC market. In 2025, a 32GB RAM kit constituted approximately 5% of a total mid-range build budget. In Q1 2026, that same component now accounts for nearly 20-25% of the total BOM.

This shift forces compromises in other critical areas:

- GPU Downgrades: Builders are allocating funds away from graphics cards to afford basic operational memory.

- Storage Sacrifices: Users are opting for smaller 500GB SSDs to offset the cost of 32GB RAM.

- Delayed Cycles: Corporate IT departments are delaying fleet refresh cycles, opting to repair rather than replace, further tightening the secondary market for parts.

Forecast: Q1–Q3 2026 Outlook

Based on current fabrication roadmaps and wafer allocation data, we project the following timeline for price stabilization:

- Q1 2026 (Current): High volatility. Prices are expected to remain elevated as retailers adjust to uncertain restocking costs.

- Q2 2026: Stabilization. We anticipate prices will plateau as the initial panic buying subsides, though significant price reductions are unlikely.

- Q3 2026: Potential Correction. New fabrication capacity in Arizona and Europe is scheduled to come online, specifically targeting the consumer DDR5 market. This influx of supply should alleviate pressure on the broader market.

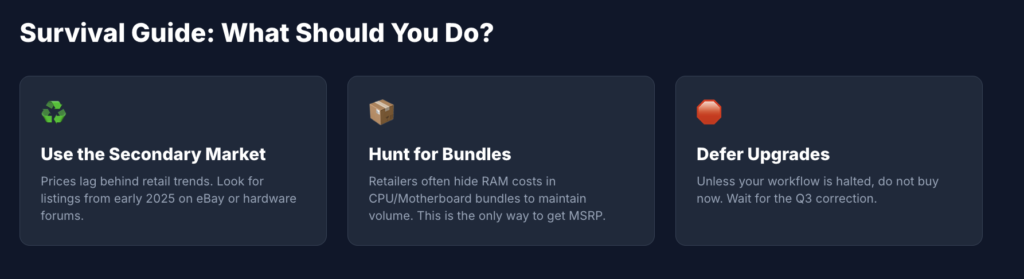

Strategic Recommendations for Consumers

Given the current market conditions, buyers should adjust their procurement strategies:

- Evaluate the Secondary Market: The most viable pricing is currently found in the used component market, where prices lag behind retail trends.

- Defer Non-Critical Upgrades: Unless essential for immediate workflows, delaying memory upgrades until Q3 2026 is recommended to avoid peak pricing.

- Prioritize Platform Bundles: Retailers often subsidize memory costs within CPU/Motherboard bundles to maintain sales volume. This remains one of the few avenues to secure memory at near-MSRP rates.

Frequently Asked Questions (FAQ)

Is it better to buy DDR4 or DDR5 right now?

From a value perspective, the price gap between DDR4 and DDR5 has narrowed significantly due to the artificial scarcity of DDR4. If you are building a new system, we strongly recommend opting for a DDR5 platform. The “legacy tax” on DDR4 means you are paying premium prices for end-of-life technology, whereas DDR5 offers future compatibility and better resale value.

Can I mix old and new RAM to save money?

While technically possible, mixing memory kits (even from the same brand) is highly discouraged in the current market. Modern memory controllers are sensitive to die variations. Mixing an older $50 kit with a new $240 kit often results in system instability or failure to boot XMP profiles, effectively negating the performance benefits of the upgrade.

Why hasn’t the price of SSDs increased as much as RAM?

While both use silicon, SSDs rely on NAND Flash, while RAM uses DRAM. The manufacturing lines for NAND and DRAM are distinct. The current shortage is specifically driven by the reallocation of DRAM lines to HBM (High Bandwidth Memory) for AI GPUs. NAND production has remained relatively stable, insulating storage prices from the same extreme volatility.

Will prices ever return to 2025 levels?

It is unlikely that we will see the sub-$50 price floor for 32GB kits in the near future. The 2025 pricing was driven by a massive oversupply glut that has since cleared. While prices will eventually drop from their current $240 peak, a “new normal” of $100-$120 for 32GB is the more probable long-term stabilization point for late 2026.